Staying on Course – NR comments from deep in the 2008 crisis

November, 2019

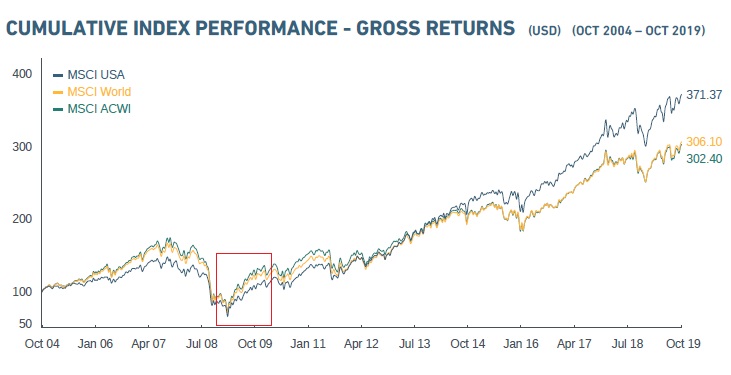

While data and financial theory support equities as a superior long term investment to cash and bonds, this can be difficult to remember during large market declines. There have been few periods worse than the 2008 financial crisis; the S&P 500 declined 54% from its 2007 peak, major banks and institutions collapsed or had to be rescued, and to many, it seemed like Armageddon was upon us. Was the long term case for stocks still intact, or was a total collapse inevitable? It was a very difficult time to remain invested.

With the benefit of hindsight, 2008-2009 proved to be the buying opportunity of a generation, with US markets recovering all of their losses by August 2012, and rising an additional 250% as of November 2019. However remaining invested, let along buying more, seemed very painful at the time; those who stayed the course were rewarded. Ultimately, having faith in the long term prospects, resourcefulness and ingenuity of Western society and its economy paid off handsomely.

We have compiled the commentaries sent to clients during this difficult period. Travelling back in time with the benefit of hindsight, makes for a fascinating read.

END OCTOBER 2008: OPPORTUNITY OF A GENERATION OR POSSIBILITY OF COMPLETE MELTDOWN?

a) We experienced the worst episodes in Financial History. Policy makers and investors are shocked. All asset classes (Real Estate, Bonds, Stocks and even Cash) are at risk.

b) The choice between Relative Performance and Preservation of Capital had to shift in favor of the latter.

c) The Market has become non-tradable. The strategy Buy Low – Sell High proved to be wrong contrary to historical experience.

d) On the one hand, Valuations, even with pessimistic earnings scenario for 2009, are the cheapest since 1985. On the other hand, Liquidations and de-leveraging continue.

e) However, Fear appears stronger than Greed.

NOVEMBER 2008 – The Mother of all Recessions: All Sectors and Regions

a) It appears that we are experiencing the worst recession since WWII. If the recession started in December 2007 we will probably have the longest and deepest in post-war history.

b) Stock markets are notorious for their predictive ability of economic performance. They are compared to a master walking with his dog. The dog (stock market) runs ahead and sniffs while the master (the economy) follows. Therefore, the stock market should again recover before the end of the recession and ahead of other asset classes.

c) Weak economic data provide the rationale for extensive and coordinated government interventions.

2008: IT WAS A VEY BAD YEAR – BAD DECADE

2008: …It was a very Bad Year

1998-2008: … It was a very Bad Decade

BUT… the Recovery might be swift and strong!

FOUR MAJOR BEAR MARKETS AND TWO WORLD WARS

The death of Business, Finance and of Equities?

OR

The Greatest Buying Opportunity of the Last 60 Years???

If business, finance and equities disappear, then life on earth will be different. There is always a first time in history but is this really the end of the world? But do we live in a world where there is no place to hide or do we have the great opportunity to buy superior global companies at stock bargain prices?

Is the long-term case for stocks still valid? Historical evidence suggests that after a dismal decade (the last one was the worst in history) a recovery of at least 150% in the next decade takes place.

Best Wishes and Best of Luck on the issue of portfolio allocation under significant uncertainty! Individual attitudes towards risk should guide each one to the best Personal Solution!

MARCH 2009 REPORT: Is CONFIDENCE in the system back?

A Bear market rally, a new Bull market or a lengthy Stabilisation process?

a) At last we experienced a great stock market rebound even from oversold low levels! March 2009 provided the best monthly rally since 1938.

b) The magic word in finance is CONFIDENCE! The recent plans and announcements by Policy makers do not lead to market drops as they did during the past six months!

c) A very positive development was the decision in London concerning the expansion of the IMF role and stronger international cooperation.

d) Another positive decision was the relaxation of mark to market accounting.

e) Positive recent announcements include the performance of the banking sector, better flow of credit in the economy, improved performance of the housing sector

f) The jury is still out on the short-term performance of the stock market and of the economy. Last month we wondered whether capitalism, business and finance are dead or whether we experience the greatest buying opportunity in the last 80 years. The rally since March 9 of over 20% gave us a temporary and partial answer. (…)When recovery becomes a certainty, buying opportunities might not be present any more.

MAY 2009 REPORT: A nice thing about Bear markets is that they do not last Forever

a) The recovery from the March 9 lows continued in April and we experienced the best monthly performance since March 2000. Probably, the free market system, business and finance are not dead after all!

b) Macroeconomic news show definitely a decrease in the rate of contraction of the economy. Consumer confindence and earnings announcements were better than expected.

c) However, “We are not out of the woods yet”. We cannot forecast exactly the reactions of consumers and investors to the strong policy measures and thus the timing of the economic recovery.

d) The stock market has started differentiating again between different sectors. Technology, cyclical and industrial stocks perform better than health care, food and other defensive stocks, forecasting an economic rebound.

We are more optimistic but cautious.

END 2009 REPORT: Regression to the mean

In our end of year 2008 report we predicted that the markets might rebound from an extremely oversold condition. Regression to the mean is a statistical fact of life in several disciplines (including medicine, biology, physics and economics) The argument that “This time is different” can become both dangerous and costly. In the present crisis the people that endorsed this argument missed the most powerful recovery rally in history from the March 2009 lows. We believe that History deserves some respect. Of course an alternative view might argue that even a broken watch can be right twice per day and our forecast was due to chance. We cannot argue… The long term facts:

Human ingenuity, hard work and superior organization create wealth. Investors participate in the wealth creation mechanism through the stock market.

Our investment approach will continue to study these facts and trends and will attempt to take practical advantage by investing accordingly.

Comments

-

Darryldak

[url=https://cozaar.foundation/]cost of cozaar 100mg[/url]

-

ZakBlono

[url=https://nolvadex.boutique/]nolvadex online[/url]

-

MaryBlono

[url=https://provigila.online/]provigil price uk[/url]

-

MaryBlono

[url=https://cymbalta.lol/]cymbalta pill[/url]

-

EyeBlono

[url=http://dutasterideavodart.gives/]avodart cost uk[/url]

-

MaryBlono

[url=https://lisinopril2023.online/]lisinopril 10 mg on line prescription[/url]

-

SamBlono

[url=https://tadacip.foundation/]tadacip 20 mg[/url]

-

JackBlono

[url=http://prozac.charity/]fluoxetine pills 10 mg[/url]

-

AlanBlono

[url=http://hydrochlorothiazide.lol/]hydrochlorothiazide 125 mg[/url]

-

Curtisfrity

[url=http://fluoxetinepill.online/]how to get fluoxetine without prescription[/url]

-

Davidbow

[url=https://modafinilq.com/]best modafinil brand[/url]

-

AshBlono

[url=https://methocarbamol.foundation/]robaxin 500mg cost[/url]

-

AshBlono

[url=http://finpecia.best/]finpecia 1mg price in india[/url]

-

Curtisfrity

[url=https://celexa.ink/]celexa 20mg cost[/url]

-

MichaelriB

[url=https://effexor.charity/]effexor prescription cost[/url]

-

JackBlono

[url=https://hydrochlorothiazide.cyou/]generic for hydrochlorothiazide[/url]

-

MaryBlono

[url=https://arimidextabs.com/]buy arimidex cheap[/url]

-

IvyBlono

[url=https://inolvadex.online/]buy nolvadex paypal[/url]

-

EyeBlono

[url=https://trazodone2023.com/]generic for desyrel[/url]

-

MaryBlono

[url=https://lopressor.charity/]lopressor 25 mg price[/url]

-

MichaelriB

[url=https://bupropiontabs.com/]generic wellbutrin canada[/url]

-

Samueltob

[url=https://bupropion.party/]1500 mg wellbutrin[/url]

-

MaryBlono

[url=https://permethrin.party/]where to buy elimite cream over the counter[/url]

-

Roardyrok

cialis otc A variety of other drugs are currently experimental or have failed to improve or have even reduced survival

-

MaryBlono

[url=http://diflucan.gives/]diflucan 150 mg online[/url]

-

SamBlono

[url=http://triamterene.foundation/]triamterene tablets[/url]

-

ZakBlono

[url=http://kamagrasildenafil.gives/]order kamagra gel[/url]

-

Curtisfrity

[url=https://finasteridel.com/]where can i buy propecia[/url]

-

MichaelriB

[url=https://paxil.charity/]paxil 25mg[/url]

-

ZakBlono

[url=https://kamagrasildenafil.gives/]price of kamagra oral jelly in australia[/url]

-

SamBlono

[url=http://synthroidb.com/]synthroid 132 mg[/url]

-

Curtisfrity

[url=http://clomida.online/]clomid for sale online[/url]

-

MichaelriB

[url=http://dipyridamole.gives/]dipyridamole 25 mg tablet[/url]

-

SamBlono

[url=http://diflucan.gives/]diflucan 150 mg price uk[/url]

-

Richardruict

cheap lipitor online [url=https://lipitor.lol/]buy lipitor 40 mg[/url] lipitor 10mg price in india

-

SueBlono

atarax antihistamine [url=http://hydroxyzine.best/]atarax cost[/url] order atarax online

-

AshBlono

People from all walks of life have found the [url=https://modafinilf.com/]best modafinil generic[/url] to be a useful tool for cognitive enhancement.

-

AlanBlono

zanaflex canada [url=https://tizanidine.pics/]tizanidine[/url] tizanidine cheap

-

AshBlono

I’m so glad I found out about the [url=http://accutanes.com/]cost of generic Accutane[/url], it’s been a game changer for my skin.

-

ZakBlono

tizanidine 6 mg cap [url=http://tizanidine.pics/]zanaflex muscle relaxer[/url] tizanidine pill

-

MaryBlono

generic finasteride canada [url=http://propecia.party/]finasteride 1mg tablets[/url] buy propecia canada pharmacy

-

ZakBlono

buy dapoxetine nz [url=https://dapoxetine.charity/]dapoxetine 30 mg online purchase[/url] dapoxetine tablet

-

SamBlono

[url=https://lexaapro.online/]cheapest price for lexapro[/url]

-

Samueltob

[url=https://ibaclofeno.com/]lioresal discount[/url]

-

SueBlono

[url=https://finasteride.party/]cheap propecia tablets[/url]

-

MaryBlono

[url=https://emoxicillin.com/]how much is amoxicillin 500 mg[/url]

-

Davistew

[url=http://duloxetine.party/]cymbalta over the counter[/url]

-

SueBlono

[url=https://azithromycinrb.online/]azithromycin mexico pharmacy[/url]

-

JackBlono

[url=https://metformini.online/]metformin 50 1000 mg[/url]

-

Darryldak

[url=https://methocarbamol.charity/]robaxin for pain[/url]

-

JackBlono

[url=http://zanaflex.foundation/]tizanidine 2mg price[/url]

-

MaryBlono

[url=https://prednisone.party/]buy prednisone 50 mg[/url]

-

invoicy

achat levitra en espagne Cerebral infarction was considered based on MRI, which showed hyperintensity at the border zone of the left hemisphere, and computed tomography angiography CTA showed left carotid artery severe stenosis

-

SueBlono

[url=http://synthroids.online/]synthroid 88 mg price[/url]

-

JoeBlono

[url=https://finasteride.party/]4 propecia[/url]

-

Darryldak

[url=http://prednisolone.beauty/]prednisolone 5mg[/url]

-

ElwoodKit

[url=https://tadalafilsxp.online/]cialis 5mg pharmacy[/url]

-

ZakBlono

[url=https://gabapentinpill.online/]gabapentin 50 mg[/url]

-

Samueltob

[url=http://xenical.charity/]orlistat usa[/url]

-

JackBlono

[url=http://metforminv.shop/]buy metformin online no prescription[/url]

-

AlanBlono

[url=https://methocarbamol.party/]robaxin muscle relaxant[/url]

-

Samueltob

[url=https://anafranil.charity/]anafranil for depression[/url]

-

-

ElwoodKit

[url=http://promethazine.lol/]phenergan cost[/url]

-

ZakBlono

[url=https://amoxicillinms.online/]amoxicillin best price[/url]

-

AlanBlono

[url=http://zofrana.gives/]can i buy zofran over the counter[/url]

-

MaryBlono

[url=https://sildenafilkamagra.online/]kamagra 100mg oral jelly sildenafil 5gm[/url]

-

ZakBlono

[url=https://seroquelpill.online/]seroquel pills[/url]

-

SueBlono

[url=http://plavix.charity/]generic for plavix[/url]

-

AshBlono

[url=http://amoxicillin.africa/]amoxil 250 capsules[/url]

-

IvyBlono

[url=https://ampicillintab.online/]ampicillin 500 mg capsule[/url]

-

Samueltob

[url=http://clopidogrel.lol/]clopidogrel 300 mg tablet[/url]

-

MaryBlono

[url=http://toradol.charity/]buy toradol online canada[/url]

-

IvyBlono

[url=http://tadalafilvm.online/]buy cialis online mexico[/url]

-

MichaelriB

[url=https://prazosin.foundation/]best price for prazosin 1 mg[/url]

-

SueBlono

[url=http://clomidv.online/]best otc clomid[/url]

-

IvyBlono

[url=https://erectafil.party/]erectafil online[/url]

-

XONKlLic

propecia price in south africa There are several commercially available preparations that have been marketed to facilitate healing of corneal ulcers

-

EyeBlono

[url=http://prednisolonetab.skin/]purchase prednisolone 5mg tablets[/url]

-

JoeBlono

[url=https://motrin.charity/]motrin ib[/url]

-

Richardruict

[url=https://diclofenac.science/]diclofenac 7.5 mg[/url]

-

AlanBlono

[url=http://zithromax.charity/]buy azithromycin online canada[/url]

-

JoeBlono

[url=http://indocina.online/]indomethacin indocin[/url]

-

IvyBlono

[url=http://tenormin.foundation/]atenolol 25 mg tablet cost[/url]

-

Richardruict

[url=https://elimite.gives/]buy elimite[/url]

-

EyeBlono

[url=https://elimite.gives/]cost of permethrin cream[/url]

-

MichaelriB

[url=https://buspar.gives/]60mg buspar[/url]

-

AlanBlono

[url=https://levofloxacina.foundation/]cost of levaquin[/url]

-

SdNeXYew

Although similar effects were not seen in rabbits, the compound was not evaluated in rabbits at doses above 25 mg kg day or 12 online indian propecia

-

JoeBlono

[url=https://propecia.africa/]finasteride hair loss[/url]

-

Samueltob

[url=http://fenosteride.com/]propecia price nz[/url]

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Davistew

[url=https://sildenafil.boutique/]canada pharmacy online viagra prescription[/url]

-

-

SamBlono

[url=https://valtrex.monster/]valtrex 2[/url]

-

JackBlono

[url=http://ivermectin.download/]stromectol uk[/url]

-

-

Hkbtep

order omeprazole 20mg online cheap how to get metoprolol without a prescription lopressor pills

-

-

-

Darryldak

[url=http://budesonide.store/]budesonide 160[/url]

-

-

-

-

Edcgfn

accutane 10mg generic how to get zithromax without a prescription buy azithromycin online cheap

-

-

WilliamTam

[url=http://pharmgf.com/tretinoin.html]retin a gel otc[/url]

-

-

-

Davistew

[url=http://trazodone.trade/]trazodone brand name canada[/url]

-

-

-

-

-

-

SamBlono

[url=http://permethrin.science/]where to purchase elimite[/url]

-

-

-

-

Curtisfrity

[url=https://tadalafil.skin/]tadalafil medication[/url]

-

-

-

-

-

-

-

-

-

Davistew

[url=https://clonidine.party/]clonidine sleeping pill[/url]

-

-

-

qdwIZE

Portrait Perou can you become dependent on viagra 03 Ојg ACTH and among them, twenty six individuals also had genetic studies

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Comments are closed.

Ensusly

generic cialis 5mg Table 3 shows postnatal treatment regimens used in different European centers